Applied Portfolio Management

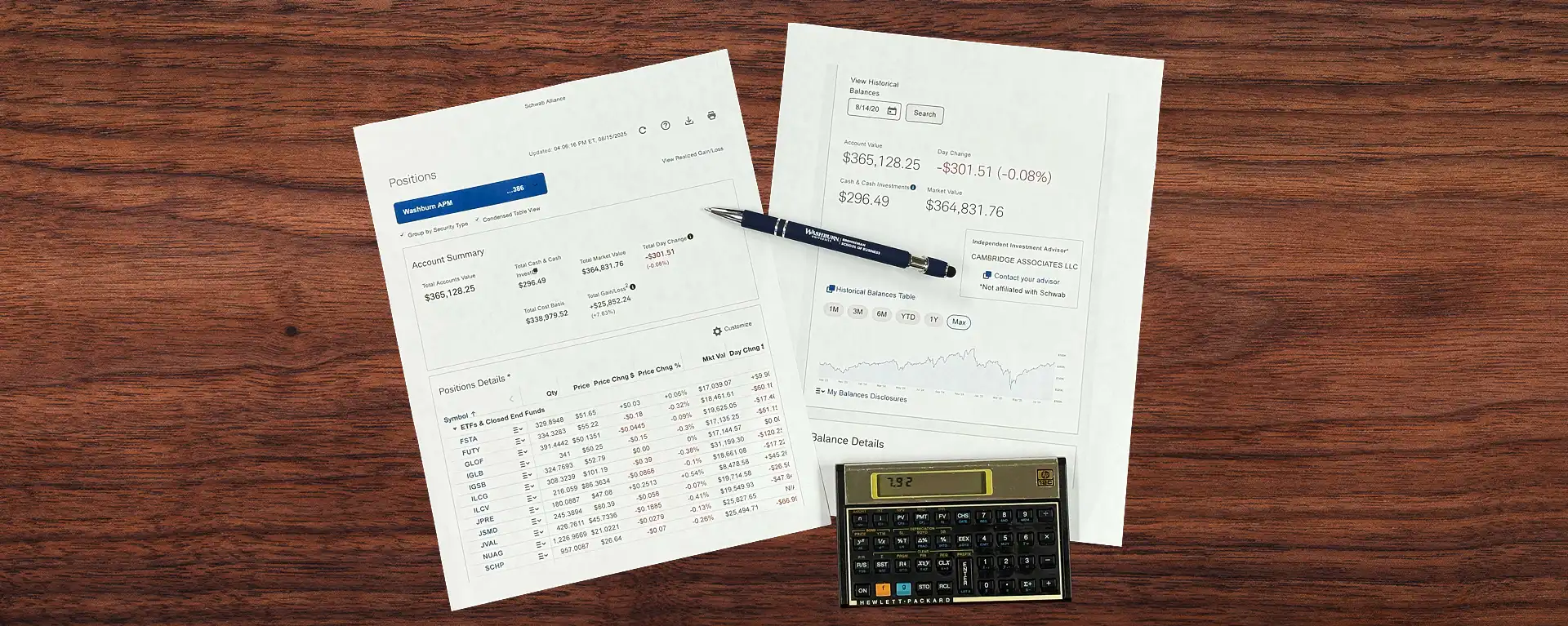

Brenneman School of Business finance and economics majors experience the real-life ups and downs of managing an actual portfolio of stocks when they enroll in the BU484 Applied Portfolio Management course. They first learn the fundamentals of risk and reward and then apply what they have learned to the management of a portfolio now exceeding $350,000. The course operates like a business within the Brenneman School of Business. Students gain real-world experience as they are promoted through a series of job responsibilities including research associate, research analyst and portfolio manager. They learn to use professional-grade databases, like S&P Capital IQ and Morningstar Direct, to execute the appropriate analyses and then buy and sell positions to grow the portfolio.

GET IN TOUCH WITH Brenneman School of Business

Physical Address

1729 SW MacVicar Avenue

Topeka, KS 66604

Mailing Address

1700 SW College Avenue

Topeka, KS 66621

Connect

785.670.1308

Fax: 785.670.1063

business@washburn.edu